Executive Summary

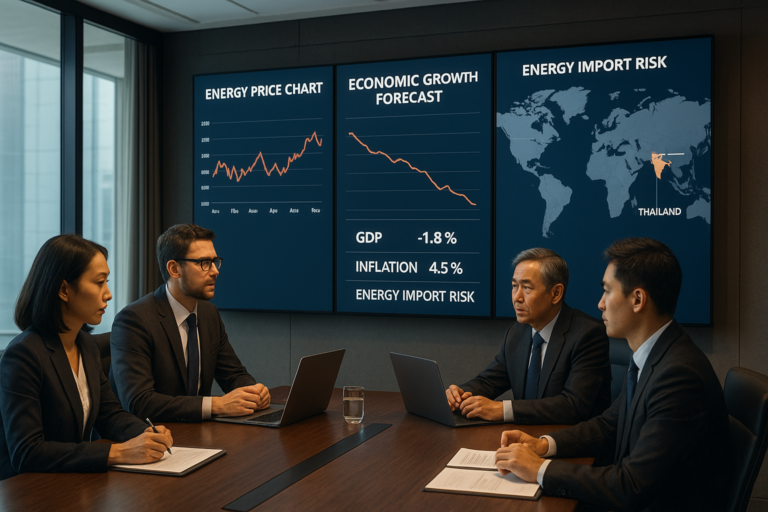

The key signal is that geopolitical tensions in Iran are crystallizing Thailand’s vulnerability as a net oil and gas importer, which translates into significant downside risks for its already moderate growth outlook and inflation trajectory. This situation matters because it directly affects Thailand’s macroeconomic stability, cost structures for businesses, and investor confidence through intensified energy price volatility and supply chain disruptions. Investors and market participants must recalibrate expectations around Thailand’s GDP growth downward, with estimates as low as 1.3%, alongside persistent inflationary pressure that erodes real incomes and corporate margins.

Key Facts

- Thailand is a major net importer of oil and gas.

- The Iran conflict is causing disruptions in energy supply and price volatility.

- Thailand’s GDP growth forecast has been revised downward to as low as 1.3% due to these disruptions.

- Inflationary pressures in Thailand are heightened as a result of increased energy costs.

Why It Matters

Thailand’s heavy reliance on imported energy makes it acutely exposed to international geopolitical shocks affecting global oil and gas supply. The Iran conflict exacerbates uncertainty and price spikes that feed directly into cost inflation across transport, manufacturing, and utilities. This can depress consumer spending power and raise operating costs for export-oriented and domestic businesses, constraining economic activity. Reduced GDP growth forecasts signal broader economic sluggishness, which in turn affects corporate earnings prospects and credit quality.

For the Thai baht, sustained energy-driven inflation and economic slowdown increase the risk of depreciation pressure, especially considering Thailand’s import bill rising amid constrained output. Currency weaknesses can feed inflation via imported goods and raise foreign currency debt servicing costs. This confluence challenges monetary and fiscal management, limiting policy room given global inflation dynamics.

Business planning and capital expenditure decisions are likely to become more cautious amid input cost volatility and uncertainty on growth. Energy-intensive sectors, including manufacturing and logistics, face margin compression. This signals that earnings estimates for listed companies within these sectors must be adjusted downward, affecting equity valuations and bond spreads. At the same time, energy importers and trading companies face heightened operational risks.

On the macro front, inflation pressure driven by energy import shocks likely undermines real wage growth and consumer confidence, restraining domestic demand. This undermines Thailand’s broader economic recovery momentum post-pandemic, impacting employment and investment climates. The downward GDP revisions underscore the fragility of Thailand’s growth model amid external shocks.

Sector Impact

Positive:

- Renewable Energy – Elevated energy security risks and high fossil fuel prices could accelerate investments and policy considerations favoring renewables and energy diversification in Thailand.

Neutral:

- Tourism – While energy cost inflation can increase operational expenses for airlines and hospitality, the core demand drivers of tourism are less directly linked to energy supply disruptions.

Risk:

- Manufacturing – Increased energy costs and supply chain uncertainty heighten production expenses and operational risk, pressuring margins.

- Transportation and Logistics – Fuel price hikes directly increase operational costs, challenging profitability.

- Retail and Consumer Goods – Inflation compresses consumer discretionary spending power, dampening sales growth.

ASEAN Context

This development appears primarily domestic in nature with limited immediate ASEAN-wide implications. However, given ASEAN countries’ shared dependence on imported energy, Thailand’s experience signals a broader regional vulnerability to Middle East geopolitical shocks. Countries with similar energy import profiles may face synchronized inflationary pressures and growth headwinds. Thailand’s adjustments and policy responses may set precedents for balancing growth and inflation risks across ASEAN.

Bottom Line

Thailand’s energy import dependence is a core macroeconomic vulnerability sharply highlighted by the Iran conflict. The combined effect of heightened inflation and downward GDP growth revisions will pressure corporate earnings, consumer spending, and currency stability. Sectoral risks center on energy-intensive industries and consumer demand-sensitive sectors. Investors must integrate these dynamics into asset allocation, recognizing energy price shocks as a material factor shaping Thailand’s near-term economic trajectory and market performance.

Thailand Investor Brief

Want deeper Thailand & ASEAN investor intelligence?